CFC: are the fines canceled or postponed?

Content of the article

Content of the article

Owners of foreign companies (Controlled Foreign Companies, or CFCs) have several obligations: submitting a notification, declaration, and report to the tax authorities and paying taxes if no exemptions apply. It is worth noting that these obligations apply to tax residents of Ukraine.

There may be situations where, for various reasons, a CFC owner fails to fulfill their obligations altogether, misses the deadlines for document submission, or provides incomplete information. In this article, we will examine the potential consequences of such actions, specifically focusing on the liability stipulated by law and the status of fines during the martial law period.

Liability

The Tax Code prescribes liability in the form of fines in cases of non-compliance or untimely fulfillment of CFC-related obligations.

These fines are calculated as a multiple of the subsistence minimum for able-bodied individuals (e.g., 100 or 300 times the subsistence minimum, etc.). Since the subsistence minimum is adjusted annually, the fines are not fixed, and their amounts increase each year. Therefore, it is essential to refer to the reporting year in which the violation occurred (e.g., 2022, 2023, 2024).

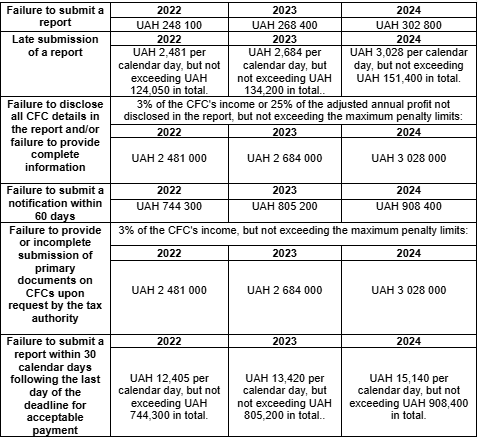

Types of violations and fines as of 2024:

- Failure to submit a report: ₴302,800.

- Late submission of a report: ₴3,028 per calendar day of delay, but no more than ₴151,400 in total.

- Failure to disclose all CFC details and/or providing incomplete information in the report: 3% of the CFC’s income or 25% of the adjusted annual profit not disclosed in the report, but not exceeding ₴3,028,000.

- Failure to submit a notification within 60 days: ₴908,400.

- Failure to provide or incomplete submission of primary CFC documents upon request by the tax authority: 3% of the CFC’s income, but not exceeding ₴3,028,000.

- Failure to submit a report within 30 calendar days following the deadline for acceptable payment: ₴15,140 per calendar day of non-submission, but not exceeding ₴908,400 in total.

In addition, taxpayers and their officials may face administrative and criminal liability for violations related to the application of CFC regulations.

In conclusion, for violations of CFC rules, the following types of liability may apply: financial (fines), administrative, and criminal. The fines are significant, and some are calculated per calendar day or instance of violation. Payment of fines is not exempt from the obligation to submit reports and documents. Given such negative consequences, we recommend avoiding violations and fulfilling obligations in advance.

Changes during martial law

The Law of Ukraine, dated May 9, 2024, No. 3706-IX, provides certain “relaxations” regarding liability. Specifically:

- No fines are applied for violations such as failure to submit or late submission of reports, failure to disclose complete information, or failure to provide notification within 60 days.

- No administrative or criminal liability is applied for violations of CFC regulations.

This “benefit” of non-application of liability is effective from January 1, 2022, throughout martial law and six months after its termination or cancellation.

It is important to note that this “cancellation of liability” is only a temporary measure. Fines, administrative, and criminal liability remain stipulated by law. However, their application and payment are postponed to a later date.

For example, if a CFC owner fails to submit a report for 2022 and martial law is lifted on January 1, 2026, no fine of ₴248,100 will be applied until June 30, 2026. Starting July 1, 2026, however, the CFC owner may receive a tax notification decision with the fine amount.

This is also related to the extended statute of limitations and tax audit periods for compliance with CFC regulations, which are set at 2,555 days (7 years). Similarly, CFC owners must retain documents (reports, copies of CFC financial statements, etc.) for the same 7-year period.

Conclusions

The obligations for CFC owners (founders, beneficiaries) have not been canceled. The application of liability and payment of fines have only been postponed. Moreover, the CFC regulations and fines could be amended and reinstated at any time.

The statute of limitations, during which tax authorities have the right to conduct inspections, is 7 years. This means it is likely that some violators will still be held accountable within this period.

We recommend avoiding law violations, keeping track of changes, and preparing in advance for the reporting tax period. Please note that the annual tax return and the following CFC report for 2024 must be submitted by May 1, 2025.

Share

Related articles

Personal data protection in different countries: GDPR, CCPA and other regimes

How to open a company abroad: a to-do list for business owners

Absolute Grounds for Refusal: Why They Are Crucial When Registering a Trademark

How to file an IRS tax return in Portugal in 2026: deadlines, rates and foreign income

We use cookies to improve the performance of the site and enhance your user experience.

More information can be found in our Privacy Notice