Term Sheet: What It Is and How to Structure an Investment Agreement

Content of the article

⚠️ Legal Disclaimer: This material is provided for informational purposes only and does not constitute legal advice. For assistance with specific legal matters, we recommend consulting a qualified legal professional.

Term Sheet (TS) is a preliminary document that may be used between an investor and a company (startup) to outline the key terms of a proposed investment before the execution of a definitive agreement. As a general rule, most provisions of a TS are not legally binding; however, it establishes the framework for subsequent negotiations and helps determine whether the parties share the same understanding of the transaction.

In practice, a Term Sheet serves as a roadmap for both founders and investors. According to the Canadian Deal Points Report (Osler, 2023), more than 97% of venture capital transactions began with the execution of a TS. It is not merely a formality, but rather an effective tool for saving time, reducing legal risks, and building trust between the parties.

Why a Term Sheet Matters

Saves time. A TS allows the parties to identify fundamental disagreements at an early stage, before investing significant time and resources into a full due diligence process and legal support.

Reduces legal risks. It outlines the parties’ basic protections, dispute resolution mechanisms, and liability for breaches of agreed terms. It also clearly defines confidentiality obligations, restrictions on parallel negotiations, and the conditions precedent to closing the transaction.

Creates a foundation for trust. A TS establishes the rules of engagement between founders and investors, creating a predictable and transparent framework for future cooperation.

10 Key Terms of a Term Sheet

Below are ten core provisions that appear in virtually every investment transaction. Understanding each of them helps founders avoid common mistakes during negotiations.

1. Valuation & Round Size

This provision determines how much capital is being invested into the business and what the company is worth before and after the transaction. A distinction is made between pre-money valuation (the company’s value before receiving the investment) and post-money valuation (the value after the investment is included). For example, if a company is valued at $4 million pre-money and raises $1 million, its post-money valuation becomes $5 million, and the investor receives a 20% equity stake.

Investor ownership formula:

Ownership Percentage = Investment Amount / Post-Money Valuation

Valuation is one of the most heavily negotiated terms and significantly affects all subsequent deal provisions.

2. Investment Instrument

The structure of an investment may vary depending on the company’s stage and the investor’s expectations:

- Common Stock – the standard option for more mature companies.

- Preferred Stock – the most common instrument in venture capital transactions; grants investors priority rights in certain situations.

- SAFE (Simple Agreement for Future Equity) – an agreement for future equity without a fixed valuation and without accruing interest; widely used at the seed stage.

- Convertible Note – a debt instrument that converts into equity during a future financing round; it has a maturity date and typically accrues interest (often 6–8% annually).

The chosen instrument determines the investor’s rights, payment priorities, and the mechanism for obtaining ownership in the company. Unlike a convertible note, a SAFE has no maturity date.

3. Liquidation Preference

This provision determines the order of payouts upon the sale or liquidation of a company. Under a standard structure, an investor holding preferred shares first recovers the invested capital (for example, a 1x preference), after which the remaining proceeds are distributed among shareholders. Some structures include participating preferred rights, allowing the investor to receive both the liquidation preference and a proportional share of the remaining proceeds.

This mechanism protects investors when the exit value is lower than expected. Founders should carefully assess preferences above 1x (e.g., 2x), as they can significantly reduce founder proceeds in an exit scenario.

4. Anti-Dilution Protection

Anti-dilution provisions apply when the company raises a subsequent financing round at a lower valuation (down round). The two most common approaches are:

- Full Ratchet – the strictest form of protection, adjusting the investor’s share price to match the new lower valuation regardless of the size of the financing. Generally unfavorable to founders.

- Weighted Average – a more balanced mechanism that takes into account the size of the new financing round. This is the market standard in most venture transactions.

These provisions help investors preserve the economic value of their ownership if the company’s valuation decreases.

5. Vesting

Vesting is a schedule under which founders and key team members gradually earn ownership of their equity over time. The market standard is a four-year vesting period with a one-year cliff. This means that if a founder leaves before completing the first year, no equity vests. After one year, 25% of the equity vests, with the remainder vesting monthly or quarterly thereafter.

This mechanism protects investors from the premature departure of key founders and contributes to team stability. Founders should also consider negotiating acceleration upon a change of control.

6. Founder Commitments and Governance Rights

These provisions define the allocation of authority between founders and investors. Key issues include board composition, protective provisions, and veto rights.

Common protected matters include:

- Amendments to the company’s constitutional documents;

- New financing rounds;

- Significant M&A transactions;

- Dividend distributions;

- Company liquidation.

The larger the investor’s ownership stake, the broader its governance rights typically become. Founders should carefully review protected matters, as an overly extensive list may hinder the company’s operational flexibility.

7. Drag-Along and Tag-Along Rights

Drag-Along Rights allow a majority shareholder or investor to initiate the sale of the company and require minority shareholders to sell their shares on the same terms. This facilitates an efficient exit process.

Tag-Along Rights allow minority shareholders to participate in a sale initiated by a majority shareholder and sell their shares on identical terms. This protects minority investors from being left behind when control of the company changes.

Right of First Refusal (ROFR) is often included alongside these provisions, giving investors the first opportunity to purchase shares before they are sold to third parties.

8. Information Rights

Information rights govern the investor’s access to company information, including periodic financial reporting (such as quarterly profit-and-loss statements and annual audits), capitalization table updates, and inspection rights.

Such transparency enables investors to identify and address potential issues promptly and is considered standard practice in professional investment transactions.

9. Conditions Precedent

Conditions precedent set out the actions that must be completed before the parties enter into the definitive investment agreements. Typical requirements include:

- Completion of legal and financial due diligence;

- Assignment of intellectual property rights to the company;

- Verification of the capitalization table and ownership structure;

- Resolution of legal issues identified during due diligence;

- Execution of NDAs and confidentiality agreements by key personnel.

The larger and more sophisticated the transaction, the more detailed these conditions tend to be. Failure to satisfy conditions precedent usually allows a party to withdraw from the transaction without legal liability.

10. Exclusivity & Costs

An exclusivity (no-shop) clause restricts the startup from negotiating with other investors for a specified period, typically between 30 and 90 days. It is one of the few provisions in a Term Sheet that is commonly legally binding. Its purpose is to provide assurance that the deal will not be undermined by parallel negotiations.

The Term Sheet also usually allocates legal and transaction costs. In most cases, each party bears its own expenses; however, investors may sometimes require the company to reimburse part of their legal fees upon successful closing of the transaction.

Jurisdiction and Arbitration: Where Should Disputes Be Resolved?

The choice of jurisdiction and arbitration institution is a strategic decision that affects not only the potential cost of dispute resolution but also investor confidence and the speed at which disputes can be resolved.

When to Keep the Jurisdiction of the Country of Incorporation

If a company operates exclusively in its domestic market and raises capital from local investors, retaining the jurisdiction of its country of incorporation is usually the simplest and most cost-effective solution. However, once a foreign investor becomes involved or cross-border M&A transactions are anticipated, it is often advisable to consider a neutral third-country jurisdiction.

International Arbitration: Advantages and Costs

International arbitration is the standard dispute resolution mechanism in transactions involving foreign investors. Its key advantage is that arbitral awards are final and binding on the parties and are enforceable in approximately 172 countries under the 1958 New York Convention.

The London Court of International Arbitration (LCIA) is one of the most widely used institutions for FinTech and startup-related disputes. According to the LCIA Annual Report 2024, 318 out of 362 cases (87%) were conducted under the LCIA Rules. The average value of disputes was USD 117,653, while the average time from filing to final award was approximately 20 months.

The overall cost of arbitration consists of administrative fees and arbitrators’ hourly rates. For high-value disputes, this hourly-rate model is often significantly more cost-effective than systems where fees are calculated as a percentage of the amount in dispute.

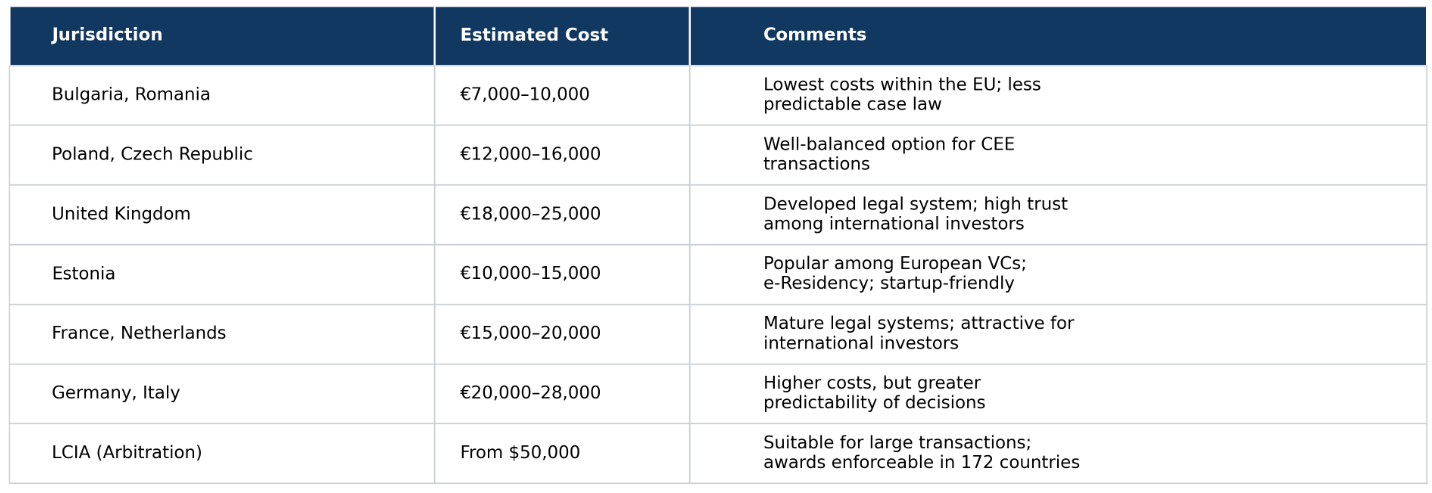

Comparative Cost of Litigation Across Jurisdictions

For reference, consider a typical dispute with a value of EUR 100,000 requiring approximately 30–50 hours of legal representation. According to data from the EU Justice Scoreboard and the OECD:

When choosing arbitration, it is also worth comparing: ICC (International Chamber of Commerce, Paris), VIAC (Vienna), and SCC (Stockholm) — all of which are reputable alternatives to the LCIA, depending on the investor’s geography and the specifics of the transaction.

Common mistakes when signing a Term Sheet

- Ignoring vesting terms. Founders sign the agreement without accelerated vesting upon a change of control — and in the event of an acquisition, they may end up with nothing.

- Overly broad list of protected decisions. This effectively gives the investor a veto over any operational action — from hiring key employees to entering into partnership agreements.

- Participating preferred without a cap. The investor receives both a preferential payout and unlimited participation in the distribution of remaining proceeds — leaving founders with very little.

- Open-ended exclusivity. The startup is blocked from engaging in other negotiations for an indefinite period, while the investor continues due diligence.

- Confusing cap table structure. Unclear equity allocations, undocumented options, or unresolved IP ownership issues can become grounds for an investor to walk away from the deal.

- Signing a term sheet without legal review. Even a “non-binding” document may include provisions that restrict founder flexibility (exclusivity, confidentiality, ROFR).

Conclusion and Next Steps

A clear Term Sheet significantly increases the chances of quickly completing and signing a full investment agreement. In practice, the most important thing is to clarify at this early stage whether both parties truly have the same understanding of the future cooperation.

Even before negotiations, founders should prepare: a complete list of all shareholders and their ownership stakes (cap table), the jurisdictional structure of the company’s registration, intellectual property documentation, and proof of clean title to the assets. A complex structure or weak legal protection framework in the country of incorporation may become a reason for an investor to отказаться from signing the term sheet.

Ukraine has strong examples: there are already at least eight unicorn companies (valued at $1B+): Grammarly, GitLab, Creatio, airSlate, People.ai, Unstoppable Domains, Rentberry, and Fintech-IT Group, which in October 2025 raised investment from UMAEF and became the first Ukrainian FinTech unicorn. In 2024, startups with Ukrainian founders raised $462 million, and in 2025 Grammarly closed a $1 billion round from General Catalyst.

A Term Sheet is only the first step. After it come a full investment agreement, potential restructuring of the corporate structure, and fulfillment of closing conditions. But without a well-drafted Term Sheet, reaching these stages becomes significantly more difficult.

Share

FAQ

1. Is a Term Sheet a legally binding document?

2. How long does it usually take to sign a Term Sheet?

3. How does a SAFE differ from a convertible note?

4. What are pre-money and post-money valuations?

5. What is the best jurisdiction for a Ukrainian startup?

6. What are drag-along rights and are they risky for founders?

7. How is a Term Sheet different from a Letter of Intent (LOI)?

8. What is vesting and why is it important for founders?

9. How much does legal support for a Term Sheet cost?

10. Can you sign a Term Sheet without a lawyer?

1. Is a Term Sheet a legally binding document?

In most cases — no. The majority of Term Sheet (TS) provisions are statements of intent and do not create legal obligations. The exception: certain clauses are legally binding — primarily exclusivity (no-shop clause) and confidentiality. Breaching them may lead to claims from the investor.

2. How long does it usually take to sign a Term Sheet?

From two weeks to two months, depending on deal complexity, the number of negotiation rounds, and jurisdiction. After signing the TS, due diligence begins — it may take another 1–3 months before the final closing of the deal.

3. How does a SAFE differ from a convertible note?

A SAFE (Simple Agreement for Future Equity) has no maturity date and does not accrue interest. It converts into shares during the next priced round or a qualifying event. A convertible note is a debt instrument with a maturity date (usually 18–24 months) and an interest rate (6–8% annually). If no new round occurs before maturity, it may become repayable as debt.

4. What are pre-money and post-money valuations?

Pre-money valuation is the company’s valuation before receiving new investment. Post-money = pre-money + investment amount. Example: $4M pre-money + $1M investment = $5M post-money. The investor receives a share equal to $1M / $5M = 20%.

5. What is the best jurisdiction for a Ukrainian startup?

It depends on target markets and investor expectations. For raising from US venture capital funds — Delaware (USA) is the standard. For European VC — Estonia (e-Residency) or the Netherlands (BV structure) are often used. For deals with international arbitration frameworks — the UK or Singapore. Each option has different administrative costs and tax implications.

6. What are drag-along rights and are they risky for founders?

Drag-along allows majority shareholders to force a company sale and require minority shareholders to join on the same terms. It is useful for exits but can be risky if investors hold majority control and can sell without founder consent. It is important to negotiate a minimum sale price (floor price) and founder consent requirements for drag-along.

7. How is a Term Sheet different from a Letter of Intent (LOI)?

An LOI is a broader document, often used in M&A transactions, outlining general intent to acquire a business. A Term Sheet is more structured and focuses on specific financial and corporate terms, typical for venture deals. In practice, the distinction is often blurred — both are preliminary, non-binding agreements.

8. What is vesting and why is it important for founders?

Vesting is the gradual acquisition of ownership rights in shares over time. It protects against situations where a co-founder leaves early but retains a large equity stake. The standard is a 4-year vesting period with a 1-year cliff. Founders should also include acceleration clauses upon change of control.

9. How much does legal support for a Term Sheet cost?

It depends on deal complexity, jurisdiction, and lawyer expertise. Legal support at the Term Sheet stage is an investment that protects founders from unfavorable terms that could become significantly more expensive later.

10. Can you sign a Term Sheet without a lawyer?

Technically — yes, since most TS provisions are not legally binding. However, in practice it is highly risky: even a single unbalanced clause (e.g., participating preferred without a cap or overly broad drag-along) can significantly reduce founder proceeds at exit. Legal support at the TS stage is much cheaper than fixing consequences after signing the full agreement.

We use cookies to improve the performance of the site and enhance your user experience.

More information can be found in our Privacy Notice