Attracting Investment in IT: Legal Aspects for Startups and Technology Companies

Content of the article

- Types of Investors: Legal Differences and Their Implications

- Legal Structure of the Company: What Investors Look For

- Key Investment Agreements: What Gets Signed and in What Order

- Team Documentation: What Should Be in Place Before Seeking Investment

- Due Diligence: What to Expect

- International Considerations: Holding Structures and Raising Foreign Investment

- Exit Mechanisms

- Investment Readiness Checklist

Content of the article

- Types of Investors: Legal Differences and Their Implications

- Legal Structure of the Company: What Investors Look For

- Key Investment Agreements: What Gets Signed and in What Order

- Team Documentation: What Should Be in Place Before Seeking Investment

- Due Diligence: What to Expect

- International Considerations: Holding Structures and Raising Foreign Investment

- Exit Mechanisms

- Investment Readiness Checklist

According to KPMG, global venture capital investment in technology companies reached USD 94 billion in 2024. In the same year, Ukraine’s IT services exports totaled USD 6.45 billion, while Ukrainian startups secured more than USD 300 million in funding from 60 venture capital funds. Behind every successful funding round, however, lies extensive legal groundwork completed long before the investment agreement is signed.

This article serves as a practical guide to the legal aspects of raising investment for startups and technology companies — from selecting the right type of investor to protecting founders’ control after closing the deal.

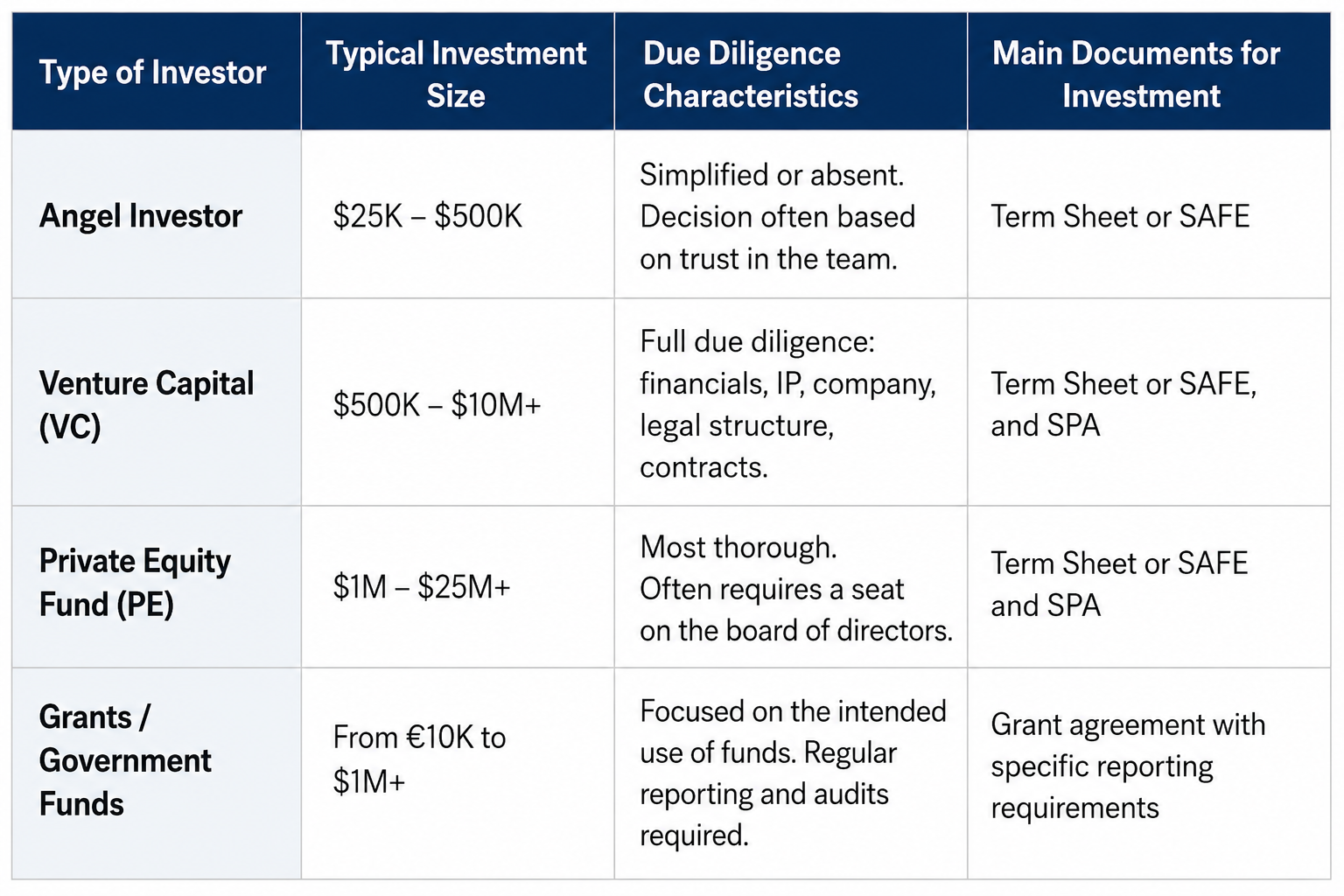

Types of Investors: Legal Differences and Their Implications

Choosing the right type of investor is not only a matter of funding amount or commercial terms. It is a strategic legal decision that determines the scope of due diligence, the volume of transaction documentation, the investor’s level of involvement in corporate governance, and, ultimately, the legal structure of the investment deal.

Angel Investors

Angel investors are the most common source of funding at the pre-seed and seed stages. According to Business Insider, the United States is home to approximately 422,000 angel investors, compared to around 3,500 venture capital funds. In Ukraine, active angel investor networks include ICLUB, United Angels Network, and Angel One, which collectively invested approximately USD 25 million in 2024.

The key advantage for founders is a relatively simple investment process. Angel investors rarely require a full corporate due diligence review. However, the main legal risk is the absence of a clear Term Sheet or other written agreement. Without properly documented terms, disputes may arise over equity ownership, voting rights, and exit expectations.

Venture Capital and Private Equity Funds

Venture capital (VC) funds typically invest from the seed stage through later growth rounds. In Ukraine, approximately 25% of venture investments in 2024 were directed toward the IT sector, particularly defense technology, which attracted around USD 1.5 billion in venture capital, according to Digital Tiger. Active investors include AVentures Capital, TA Ventures, Digital Future, CIG, and ICU Ventures.

From a legal perspective, working with VC funds involves a structured and often lengthy negotiation process. Due diligence generally takes 4–12 weeks, covering financial, legal, operational, and intellectual property matters. Investment agreements commonly provide the fund with a seat on the supervisory board or board of directors, resulting in a meaningful reduction of the founders’ operational autonomy after the transaction closes.

Grants and Government Funding Programs

Grant financing is non-dilutive, meaning founders retain full ownership of their equity. Its primary disadvantage is the strict reporting obligations and the requirement to use funds exclusively for approved purposes.

The main funding programs available to Ukrainian startups include the Ukrainian Startup Fund, Ukrainian Future Fund, Horizon Europe (EU), SBIR/STTR (United States), and Diia.City. According to market estimates, these programs provided approximately USD 5–6 billion in grant funding to startups during 2024–2025.

An important legal consideration is that receiving funding from international programs such as Horizon Europe requires compliance not only with technical eligibility criteria but also with legal requirements. Applicants generally need a properly registered legal entity in an eligible jurisdiction, a transparent ownership structure, and the absence of conflicts of interest.

Legal Structure of the Company: What Investors Look For

2.1. Legal Entity Types in Ukraine

In Ukraine, the most common legal structures for IT startups are the Limited Liability Company (LLC) and, far less frequently, the Joint Stock Company (JSC), whether Private (PrJSC) or Public (PJSC).

An LLC is the preferred legal form for most startups. It offers limited liability for shareholders, a relatively simple incorporation process, straightforward procedures for changing ownership, and significant flexibility in determining governance rules through the company’s charter. For these reasons, an LLC is the standard choice for companies raising early-stage investment.

A Joint Stock Company (JSC) is generally more suitable for businesses planning to raise substantial capital through the issuance of shares or preparing for an Initial Public Offering (IPO). In Ukraine, however, issuing securities requires registration and compliance with the regulations of the National Securities and Stock Market Commission (NSSMC). These regulatory requirements make the JSC structure significantly more complex and costly for early-stage fundraising.

2.2. Why Corporate Structure Matters to Investors

Before signing an investment agreement, venture capital funds and angel investors carefully examine the company’s ownership and legal structure. An unclear or overly complicated corporate structure is often considered a major red flag during due diligence.

The most common issues that can delay or prevent an investment include:

- Intellectual property rights have not been properly assigned and remain owned by individual developers rather than the company.

- Founders’ equity arrangements are reflected only in the company’s charter, without a shareholders’ agreement or other corporate documentation.

- Previous financing arrangements, loans, or informal agreements affecting the company’s capitalization have not been properly documented.

- Multiple legal entities operate without a clearly defined allocation of functions, creating a fragmented group of companies instead of a coherent holding structure.

According to the European Patent Office (EPO) and the European Union Intellectual Property Office (EUIPO), startups that have registered an EU trademark are 6.1 times more likely to attract investment. Similarly, startups holding a European patent are 5.3 times more likely to secure funding.

These figures demonstrate that properly protecting intellectual property is not merely a legal formality—it is a key factor influencing a company’s valuation and attractiveness to investors.

Key Investment Agreements: What Gets Signed and in What Order

Raising investment involves a sequence of legal documents, each reflecting a different stage of the negotiations and a different level of commitment. Understanding how these documents fit together helps founders avoid common pitfalls and negotiate from a position of knowledge.

3.1. Term Sheet (TS)

A Term Sheet is a preliminary document outlining the key commercial terms of a proposed investment, including the company’s pre-money valuation, the investment amount, the investor’s equity stake, voting rights, exit mechanisms, and protective provisions.

Although a Term Sheet is generally non-binding, certain clauses—such as exclusivity and confidentiality—are typically legally enforceable.

A well-drafted Term Sheet is important because it establishes the framework for all subsequent negotiations. The terms agreed at this stage are highly likely to be reflected in the Share Purchase Agreement (SPA) and the Shareholders’ Agreement (SHA). By signing a Term Sheet without proper legal review, founders effectively accept the commercial framework of the entire transaction.

3.2. Share Purchase Agreement (SPA)

The Share Purchase Agreement (SPA) is the principal legally binding document governing the investment transaction. It specifies:

- the number or percentage of shares being transferred to the investor;

- the purchase price and payment structure (lump sum, installments, or milestone-based payments);

- representations and warranties provided by the founders regarding the company’s legal and financial status, including the absence of litigation, ownership of intellectual property, and regulatory compliance;

- indemnification provisions establishing compensation mechanisms if those representations prove inaccurate;

- closing conditions, specifying the actions that must be completed before the transaction is finalized.

For founders, the representations and warranties section is often the most sensitive part of the SPA. Broadly drafted warranties may expose founders to investor claims long after the investment has closed.

3.3. Shareholders’ Agreement (SHA)

The Shareholders’ Agreement (SHA) governs the relationship between shareholders after the investment is completed. Its key provisions typically include:

- the composition and authority of the company’s governing bodies, including the board of directors, executive management, quorum requirements, and veto rights;

- Right of First Refusal (ROFR), requiring a shareholder wishing to sell shares to first offer them to existing shareholders on the same terms;

- Tag-Along Rights, allowing minority shareholders to participate in a sale initiated by the majority shareholder under identical terms;

- Drag-Along Rights, enabling majority shareholders to require minority shareholders to participate in the sale of the company under the same conditions;

- dividend distribution policies and exit mechanisms, including IPOs, trade sales, and share buy-backs;

- deadlock resolution procedures, defining how disputes are resolved when shareholders cannot reach agreement.

3.4. SAFE (Simple Agreement for Future Equity)

The SAFE was developed by Y Combinator as a financing instrument that enables startups to raise capital without determining the company’s valuation at the time of investment.

Under a SAFE, investors provide funding today in exchange for the right to receive equity during a future qualified financing round or upon an IPO, typically benefiting from either a discount rate or a valuation cap.

The primary advantages of SAFE agreements are speed, simplicity, and reduced legal costs. They also eliminate the need to negotiate a company valuation at an early stage.

However, a SAFE is neither equity nor debt. Until conversion, investors generally do not receive voting rights. Founders should also recognize that issuing multiple SAFEs can lead to substantial equity dilution when they eventually convert.

3.5. SAFT (Simple Agreement for Future Tokens)

A SAFT is the blockchain equivalent of a SAFE. Instead of future equity, investors receive the contractual right to obtain digital tokens once the protocol or platform is launched.

Compared with direct token sales, SAFTs operate within a more structured legal framework. In many jurisdictions, they are treated as securities, requiring either regulatory registration or reliance on available exemptions, such as Regulation D (Reg D) in the United States.

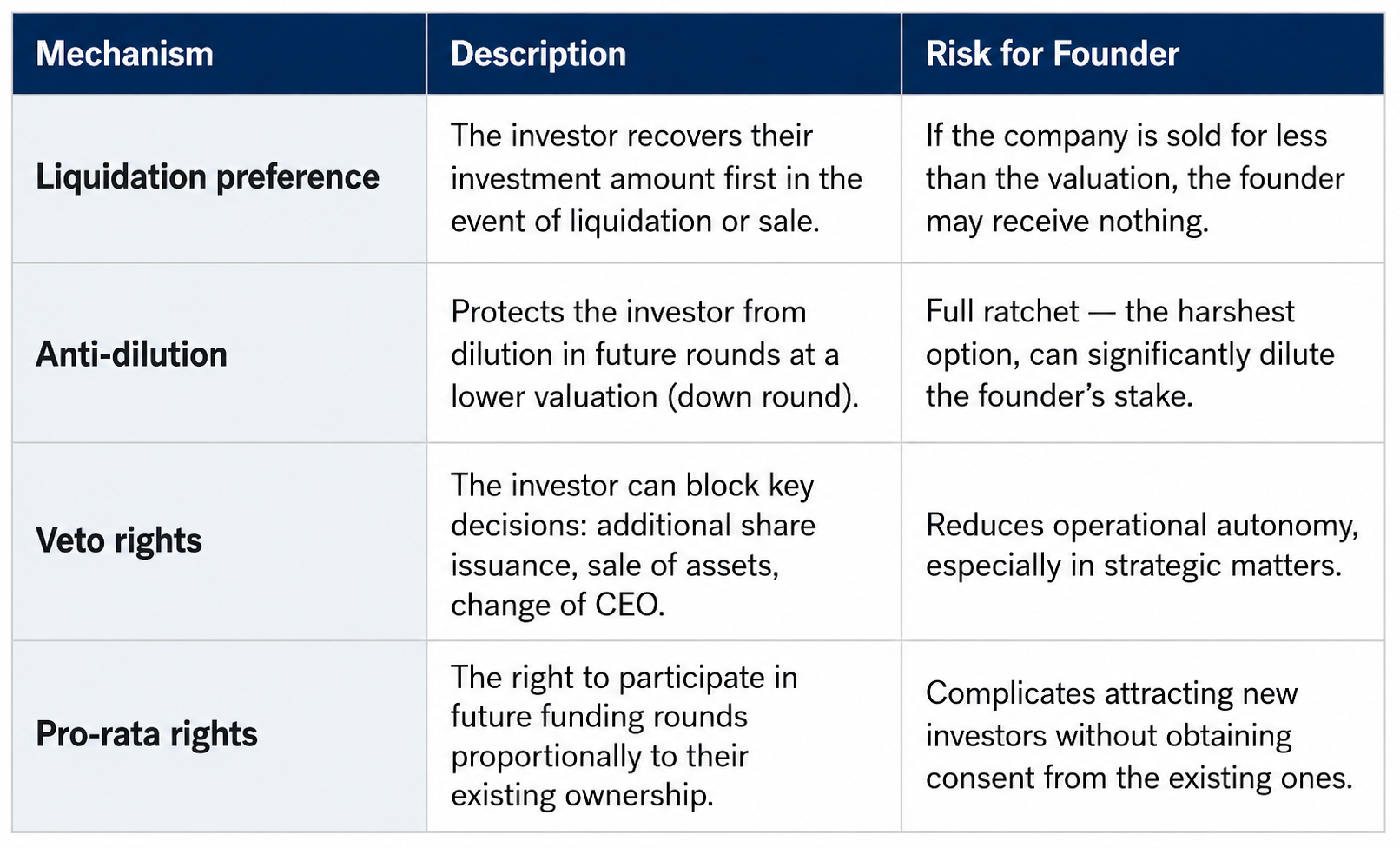

3.6. Investor Protection Mechanisms: What Founders Should Understand

Virtually every investment agreement contains provisions designed to protect the investor’s interests. Before signing any transaction documents, founders should clearly understand the legal and commercial implications of these protective mechanisms.

Team Documentation: What Should Be in Place Before Seeking Investment

Investors evaluate more than just the product and financial performance—they also assess the team. Internal corporate governance and employment relationships should be properly documented before investment negotiations begin. Any unresolved issues between co-founders are considered a significant red flag during due diligence.

4.1. Founders’ Agreement and Equity Allocation

Before raising external capital, the founders should enter into a written agreement covering the following key matters:

- Equity ownership and vesting schedule. The market standard is a four-year vesting period with a one-year cliff, meaning founders earn their equity gradually over four years. If a founder leaves before completing the first year, they typically forfeit their unvested shares.

- Roles and responsibilities of each founder (e.g., CEO, CTO, CPO).

- Deadlock resolution procedures for disputes between founders.

- Share buy-back mechanisms and Right of First Refusal (ROFR) provisions governing the transfer of shares when a founder exits.

- Non-compete and non-solicitation obligations.

4.2. Securing Intellectual Property Rights

This is one of the most overlooked yet most critical issues from an investor’s perspective.

If software code, algorithms, or other key technology were created by freelance developers or employees without properly assigning intellectual property rights to the company, the transaction may be delayed—or even blocked—during due diligence.

To avoid this risk, startups should ensure that:

- all developers, contractors, and consultants have signed Intellectual Property Assignment Agreements (IP Assignment Agreements) transferring ownership of created IP to the company;

- employment agreements contain work-made-for-hire or employee invention assignment provisions confirming that intellectual property created within the scope of employment belongs to the employer;

- licenses for third-party software have been reviewed to ensure compatibility with the commercial product, particularly where copyleft open-source licenses are involved;

- key brands are protected through trademark registration, and core technologies are protected through patents, where appropriate.

4.3. Employee Stock Option Plan (ESOP)

An Employee Stock Option Plan (ESOP) is a long-term incentive program that allows key employees to acquire equity in the company through stock options.

Investors commonly require the company to establish—or commit to establishing—an option pool before closing the investment round. This pool typically represents 10–20% of the company’s fully diluted share capital.

Founders should understand that the option pool generally dilutes their ownership, rather than the investor’s. As a result, both the size of the pool and the timing of its creation are often important negotiation points during the investment process.

Due Diligence: What to Expect

Due diligence (DD) is the comprehensive review conducted by an investor before closing an investment transaction. For IT startups, the process typically consists of three parallel workstreams.

5.1. Legal Due Diligence

The legal review usually covers:

- Corporate documentation: the company’s charter, shareholder register, board and shareholder resolutions, and shareholders’ agreement.

- Intellectual property rights: ownership of source code, trademarks, patents, and confirmation that all team members have signed IP Assignment Agreements.

- Commercial contracts: agreements with customers, contractors, and suppliers; the existence of Non-Disclosure Agreements (NDAs); and any exclusivity obligations.

- Employment matters: employment agreements, stock option plans (ESOP), and confirmation that there are no undisclosed employment disputes.

- Regulatory compliance: compliance with GDPR (where the company has EU users), licensing requirements, and industry-specific regulations.

- Litigation: any ongoing or potential legal claims and disputes involving the company.

5.2. Financial Due Diligence

The financial review generally includes:

- an audit or review of financial statements covering the previous two to three years;

- analysis of the company’s cost and revenue structure, including burn rate, runway, and unit economics;

- verification of tax compliance and the absence of outstanding tax liabilities;

- review of the company’s capitalization table (cap table), including the current ownership structure, outstanding SAFEs, and convertible notes.

5.3. Technical Due Diligence

The technical assessment focuses on:

- the quality, maintainability, and security of the source code;

- the product’s architecture and scalability;

- dependencies on third-party software and compliance with open-source licensing requirements;

- the development team and software engineering processes.

Practical Tip

Prepare a data room before beginning investor discussions. A data room is a structured repository containing all legal, financial, and technical documents that investors will review during due diligence.

A well-organized data room significantly accelerates the due diligence process and creates a strong first impression of the company’s professionalism and investment readiness.

International Considerations: Holding Structures and Raising Foreign Investment

6.1. Should You Raise Investment in Ukraine or Through a Foreign Company?

When attracting foreign investors—particularly venture capital funds based in the European Union or the United States—raising capital directly through a Ukrainian legal entity may complicate the transaction for several reasons.

- A foreign individual investing in a Ukrainian Limited Liability Company (LLC) must register as a Ukrainian taxpayer, obtain a Tax Identification Number (TIN), and comply with local tax reporting requirements. This process can take several weeks and involves additional administrative costs.

- Dividend repatriation from Ukraine remains subject to certain foreign exchange restrictions, particularly during martial law.

- Most international venture capital funds use standardized investment documentation designed for Delaware C-Corporations or UK companies. Adapting these documents to a Ukrainian LLC often requires additional legal work and increases transaction costs.

6.2. Multi-Holding Structure

The most common solution for Ukrainian technology startups raising international capital is a multi-holding structure, which typically consists of three layers.

Top Holding Company (TopCo)

The parent company is incorporated in a jurisdiction with a well-developed venture capital ecosystem. The most popular options include:

- Delaware C-Corporation (United States) — the market standard for U.S. venture capital investment;

- United Kingdom — commonly used for companies targeting international markets;

- Estonian OÜ (through the e-Residency program) — a popular choice for startups focused on the European Union.

Operating Company (OpCo)

The operating company remains in Ukraine (or another jurisdiction, such as an EU Member State). It serves as the employer of the development team, enters into customer agreements, and conducts the company’s day-to-day business operations.

IP Holding Company (IP HoldCo) (Optional)

Some startups establish a separate company to own intellectual property, including trademarks, patents, and software. The IP HoldCo licenses these assets to the operating company, providing additional asset protection and, in certain circumstances, potential tax planning benefits.

When implementing a multi-holding structure, founders should also consider Ukraine’s Controlled Foreign Company (CFC) rules, transfer pricing regulations, and applicable foreign exchange legislation.

6.3. Dividend Distribution and Reinvestment

Ukraine’s Double Taxation Agreements (DTAs) determine the withholding tax applicable to cross-border dividend payments.

While the standard Ukrainian withholding tax on dividends is 15%, the applicable DTA may reduce this rate to 5–10%, depending on the jurisdiction and the ownership structure.

Holding structures established in jurisdictions such as Estonia or the Netherlands may lawfully reduce withholding tax exposure. However, these benefits are generally available only where the holding company has sufficient economic substance in the relevant jurisdiction, rather than serving as a purely nominal entity.

Exit Mechanisms

Investors always think about their exit strategy. Founders should understand this from the outset and ensure that exit mechanisms are clearly addressed in the investment documentation.

Initial Public Offering (IPO)

An Initial Public Offering (IPO) involves listing the company’s shares on a public stock exchange. It requires extensive preparation, financial audits, regulatory compliance, and corporate restructuring. Although it typically offers the highest potential return, it is also the longest-term and most demanding exit option.

Trade Sale

A trade sale is the sale of the company to a strategic acquirer, such as a larger corporation operating in the same or a related industry. This is the most common and realistic exit route for Ukrainian technology startups.

Buy-Back

Under a buy-back, the company or its founders repurchase the investor’s shares. This option generally requires sufficient available capital or the ability to secure additional financing to fund the repurchase.

Secondary Sale

A secondary sale occurs when an investor sells their shares to another investor rather than back to the company. The Shareholders’ Agreement (SHA) should clearly regulate such transactions through provisions such as the Right of First Refusal (ROFR) and Tag-Along Rights to protect the interests of all shareholders.

Investment Readiness Checklist

Corporate Structure

- The appropriate legal structure has been established (either a Ukrainian LLC or a foreign holding company).

- Equity ownership among the founders has been documented in writing, including a vesting schedule.

- The capitalization table (cap table) has been modeled for the next two to three funding rounds.

- An Employee Stock Option Plan (ESOP) has been established or planned.

Intellectual Property

- Ownership of the source code, trademarks, patents, and databases has been properly assigned from individuals to the company.

- IP Assignment Agreements have been executed with all developers and contractors.

- Trademarks have been registered in the relevant target jurisdictions (e.g., EUIPO, USPTO, or through the Madrid System).

- Open-source software licenses have been reviewed to ensure compatibility with the company’s commercial product.

Internal Documentation

- A Founders’ Agreement or Shareholders’ Agreement (SHA) has been executed between the co-founders.

- Non-Disclosure Agreements (NDAs) have been signed with employees and key contractors.

- Core commercial agreements, including Master Service Agreements (MSAs), Service Level Agreements (SLAs), and public terms of service, have been prepared.

- A Privacy Policy and Terms of Use have been published on the company’s website to support compliance with GDPR where applicable.

Due Diligence Readiness

- A well-organized data room has been prepared.

- Financial statements covering the previous two to three years are available.

- There are no unresolved litigation matters or material legal claims.

- Compliance with GDPR, licensing requirements, and other applicable regulatory obligations has been confirmed.

Successful fundraising by Ukrainian technology companies demonstrates the importance of thorough legal preparation. Notable examples include Preply, which raised USD 120 million in 2022 to expand its AI capabilities; People.ai, which achieved unicorn status following a USD 100 million funding round in 2021; and Grammarly, which secured USD 1 billion from General Catalyst in May 2025 without issuing additional equity.

Each of these transactions illustrates the same principle: successful fundraising is built not only on an innovative product, but also on years of careful legal structuring, corporate governance, and well-managed investor relationships.

Share

FAQ: Frequently Asked Questions About Raising Investment in IT Answers to the questions we most frequently receive from startup founders and technology companies.

Where should I start when preparing to raise investment?

How is a SAFE different from a convertible note?

What is a liquidation preference, and why does it matter?

Can we raise investment without incorporating a company abroad?

How much equity should be given to an investor in a seed round?

What is vesting, and why do investors require it for founders?

How can we protect the rights to our source code if it was developed by freelancers?

What is a down round, and how does it affect founders?

Can a company raise investment through tokens or cryptocurrency?

Do you need a lawyer when signing a Term Sheet if it is "non-binding"?

Where should I start when preparing to raise investment?

Start with a legal and corporate review of your company's current state, ideally before approaching investors rather than in parallel with the fundraising process. The legal audit should cover the ownership structure, the proper assignment of intellectual property rights, internal agreements between the founders, and contracts with customers and team members. At the same time, you should prepare a well-organized data room and a financial model. Approaching investors with an incomplete legal structure often results either in failing due diligence or in receiving less favorable investment terms than would otherwise be possible. Approaching investors with an incomplete or poorly structured legal framework significantly increases the likelihood of either failing due diligence or receiving less favorable investment terms than would otherwise be possible.

How is a SAFE different from a convertible note?

Both instruments allow startups to raise capital without determining the company's valuation at the outset and convert into equity at a later stage. The key difference is that a convertible note is a debt instrument: it carries an interest rate and a maturity date. If the conversion does not occur, the investor may demand repayment of the funds. A SAFE is not debt. The investor generally has no right to demand repayment and simply waits for the investment to convert into equity upon the occurrence of the agreed triggering event. For founders, a SAFE is considered less risky, while a convertible note gives investors greater legal leverage if the next funding round is delayed.

What is a liquidation preference, and why does it matter?

A liquidation preference gives an investor the right to recover their investment (or more) before other shareholders in the event of a liquidation, sale, or other exit of the company. For example, a 1x non-participating liquidation preference means the investor first receives an amount equal to their original investment, after which the remaining proceeds are distributed among all shareholders on a pro rata basis. A 2x liquidation preference entitles the investor to receive twice the amount of their investment before any remaining proceeds are distributed. A participating liquidation preference ("double dip") allows the investor to first recover their investment and then also participate in the distribution of the remaining proceeds. Founders should always model the waterfall to understand how proceeds will be distributed under different exit scenarios.

Can we raise investment without incorporating a company abroad?

Technically, yes. Legally, there are certain limitations. Most foreign venture capital funds have internal investment restrictions based on jurisdiction, and many are unable to invest directly in Ukrainian limited liability companies (LLCs). These restrictions are generally less significant for angel investors and grant funding programs. If your goal is to attract investment from a U.S. or UK venture capital fund, establishing a holding company in Delaware or the United Kingdom can significantly improve your chances and simplify the investment process. However, the decision to incorporate abroad should take into account Controlled Foreign Company (CFC) rules, foreign exchange regulations, and the ongoing operational costs of maintaining the corporate structure.

How much equity should be given to an investor in a seed round?

The generally accepted market range for a seed round is 5% to 15% equity. Giving up more than 25–30% should be viewed as a serious warning sign, as founders risk losing majority control after subsequent funding rounds. It is important to model not just the current financing round, but the company's entire capitalization table, taking into account the employee stock option pool (ESOP), future SAFEs, and the Series A round. In some cases, founders intentionally agree to give a larger equity stake in exchange for a strategic investor, mentorship, or market access—but this should be a well-considered decision rather than the result of unprepared negotiations.

What is vesting, and why do investors require it for founders?

Vesting is a mechanism under which founders earn their equity gradually over a specified period of time. The market standard is four-year vesting with a one-year cliff. If a founder leaves the company before the cliff period ends, they receive no equity. After the cliff, ownership vests gradually over the remainder of the vesting period. Investors require vesting to protect the company from a situation where a founder leaves shortly after the investment round closes while retaining a substantial equity stake despite making no further contribution to the business. It is important for founders to understand that vesting does not mean they are not shareholders—it means their right to the full equity interest is acquired over time.

How can we protect the rights to our source code if it was developed by freelancers?

You should sign an IP Assignment Agreement with every freelancer or contractor—a document that expressly transfers all rights to the source code, designs, and other work products created by the contractor to the company. By default, in most jurisdictions, including Ukraine, copyright in a work (and source code is protected by copyright) belongs to its author unless otherwise expressly provided by contract. Therefore, the absence of an IP Assignment Agreement creates a legal risk, as the freelancer may technically retain ownership rights to the work. During due diligence, investors will verify that such agreements have been executed with all contributors.

What is a down round, and how does it affect founders?

A down round is a financing round in which the company's valuation is lower than it was in the previous round. This is a challenging situation because new shares are issued at a lower price, automatically reducing the ownership percentage of all existing shareholders. If an earlier investor benefits from full ratchet anti-dilution protection, their ownership is preserved at the founders' expense. Weighted average anti-dilution is generally considered a more balanced approach. A down round can also damage the company's reputation, making future fundraising more difficult. The best way to reduce this risk is to avoid overvaluing the company in early funding rounds and to build realistic financial projections.

Can a company raise investment through tokens or cryptocurrency?

Yes, but doing so involves significant regulatory considerations. The primary fundraising mechanisms are SAFTs (Simple Agreements for Future Tokens) and direct ICOs (Initial Coin Offerings) or IDOs (Initial DEX Offerings). In most jurisdictions, tokens are classified either as security tokens or utility tokens, and this classification determines the applicable regulatory framework. In the European Union, the Markets in Crypto-Assets Regulation (MiCA) establishes a harmonized legal framework for the issuance of crypto-assets. In the United States, the Securities and Exchange Commission (SEC) continues to apply the Howey Test to determine whether a token qualifies as a security. In 2025, raising capital through tokens without appropriate legal advice presents a significant regulatory risk.

Do you need a lawyer when signing a Term Sheet if it is "non-binding"?

Yes—and this is one of the most important recommendations. Although a Term Sheet is generally non-binding with respect to its commercial terms, it establishes the legal framework for all subsequent transaction documents, including the Share Purchase Agreement (SPA), Shareholders' Agreement (SHA), and Employee Stock Option Plan (ESOP). In practice, the terms agreed in the Term Sheet are extremely difficult to renegotiate at the SPA stage without creating significant conflict. Engaging a lawyer at the Term Sheet stage is therefore not simply an expense, but a safeguard against accepting provisions whose long-term implications may not be fully understood. Key terms such as liquidation preference, anti-dilution protection, Right of First Refusal, drag-along rights, and the size of the option pool are typically negotiated in the Term Sheet, and each of them directly affects how much value founders ultimately receive upon a successful exit.

Related articles

Compliance and Privacy (GDPR & Data Protection): compliance is not about paperwork, but about customer trust

Rights to an IT Product: How to Transfer Past IP Rights and Set Up Future Assignments

Preparing for investment deals: steps for IT companies

How to protect your intellectual property rights online if your brand or product is being copied?

We use cookies to improve the performance of the site and enhance your user experience.

More information can be found in our Privacy Notice